17 March 2026

This Week’s Cost Intelligence

Construction cost movement across the GCC remains selectively inflationary, driven primarily by energy-linked materials and polymer-based inputs. Bitumen has recorded a significant increase (+19.03%) week-by-week, while polyvinyl continues to show upward momentum, reflecting sustained demand within infrastructure and MEP-related systems. In contrast, key metals such as zinc, copper, and platinum have softened, indicating localized corrections within global commodity markets.

Freight and logistics conditions remain volatile rather than easing, influenced by ongoing geopolitical tensions in the Middle East, particularly across critical shipping routes. While certain indices show short-term stabilisation, underlying risks linked to fuel pricing and insurance premiums continue to place upward pressure on landed material costs.

Overall, the market is stable but reactive, with procurement risks concentrated in specific material categories rather than across the entire construction supply chain.

Stonehaven Cost Index (SCI)

This Week's Material Takeaways

Driver Note

Material Movement This Week

Data as of 17th March 2025 - 17th March 2026

To view the price fluctuations in detail, please download our latest dataset below.

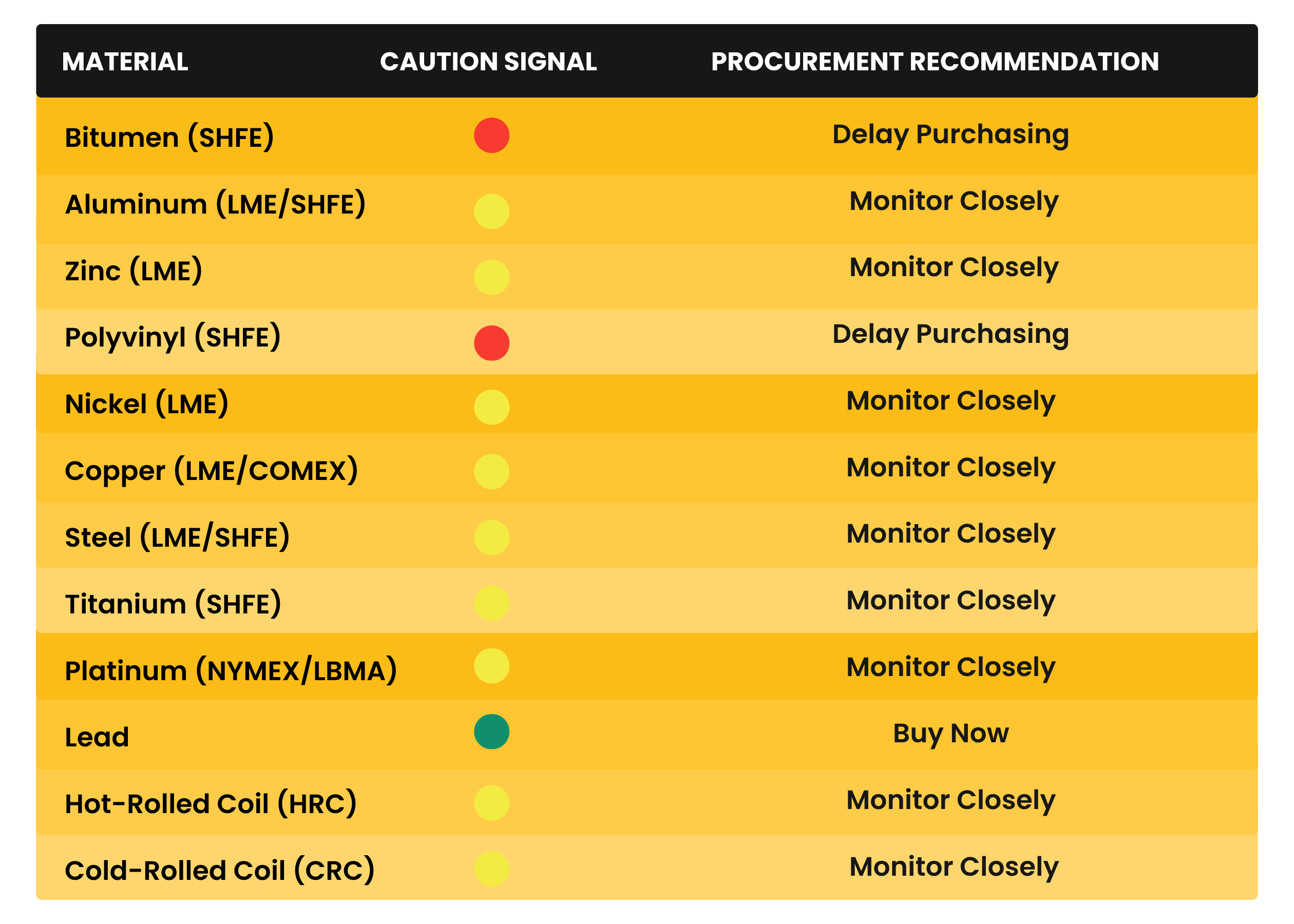

Market Material Watchlist

Material Movement & Cost Implications

This week’s material trends highlight a divergence between energy-driven materials and industrial metals:

-

Upward Pressure:

-

Bitumen (+19.03%) – driven by fuel costs and infrastructure demand

-

Polyvinyl – reflecting strong demand in construction and utilities

-

-

Stabilising / Neutral:

-

Steel (LME/HRC/CRC) – moderate and controlled movement

-

Aluminium – showing early signs of softening

-

-

Downward Correction:

-

Zinc, Copper, Platinum – indicating easing industrial demand and improved supply conditions

-

Our Commercial Interpretation

Cost escalation is not broad-based. It is concentrated in energy-sensitive and polymer-linked materials, allowing selective procurement strategies rather than overall cost inflation adjustments.

Currency & Inflation Lens

AED vs Key Trading Currencies

*Data as of 17th March 2026

SAR vs Key Trading Currencies

*Data as of 17th March 2026

Stonehaven Analysis

Most major currencies (EUR, GBP, JPY, CNY, SGD) have weakened against both AED and SAR, reflecting a relatively stronger position of GCC currencies due to their USD peg.

The Indian Rupee (INR) has shown slight strengthening, while the Australian Dollar (AUD) has remained broadly stable with marginal weakening. Overall, this creates a generally favourable import environment, particularly for materials sourced from Europe and Asia.

Impact on Construction Costs

1. Imported Materials

A stronger AED and SAR improve purchasing power for imported materials, particularly from Europe and Asia.

Impact:

-

Supports moderate reduction in landed material costs

-

Enhances competitiveness in contractor pricing, particularly for steel, finishes, and MEP components

-

Benefit remains currency-driven and limited, not a structural cost reduction

2. Currency Risk

Current FX movements are favourable but remain volatile and externally driven (USD strength, macro conditions).

Impact:

-

No immediate adjustment required to cost plans

-

Continued monitoring recommended, particularly for long-duration procurement packages

-

Avoid premature escalation allowances based solely on short-term FX movement

Overall Market Position

Currency movements are currently providing a natural offset against inflationary pressures from energy and logistics. However, the benefit is incremental rather than transformative.

Summary:

-

Materials: Slight cost advantage (import-driven benefit)

-

Overall: Stable with marginal cost relief, not a full cost correction

Global Inputs & Freight Benchmarks

Logistics & Freight – Construction Cost Multipliers

*Data as of 17th March 2026

How Do Shipping Indices Impact the Construction Industry due to Middle East Conflicts?

-

Material Costs

Conflicts in the Middle East, particularly disruptions in key shipping routes, have led to fluctuations in shipping indices causing increased transportation costs and higher material prices, which impact construction project budgets. -

Shipping Routes and Delays

Conflicts affecting critical shipping lanes like the Suez Canal and the Strait of Hormuz, can cause disruptions such as delays, rerouted ships, and higher insurance premiums, directly impacting lead times for construction materials and potentially delaying project completion dates. -

Increased Freight and Insurance Costs

Increased fuel prices and shipping insurance premiums are causing shipping companies to charge higher rates or opt for longer, safer routes, which is reflected in the Global Container Freight Index, leading to increased costs for construction materials and equipment, thereby raising project expenses. -

Supply Chain Disruptions

The Middle East conflict has also started causing delays and material shortages, which are reflected in shipping indices leading to increased procurement costs and significant delays for construction projects reliant on these critical lanes. -

Impact on Bulk Commodities

Ongoing conflicts in the Middle East have led to rising oil prices and shipping disruptions, causing increased shipping rates for bulk materials like steel, coal, and iron ore, which directly impact construction costs, budgets, and project timelines. -

Impact on Fuel Prices and Energy Costs

Rise in oil prices due to regional instability or disruptions in the oil supply chain directly impacts shipping rates. Since the shipping industry is highly dependent on fuel, an increase in fuel costs will raise the overall cost of transporting goods, including construction materials.

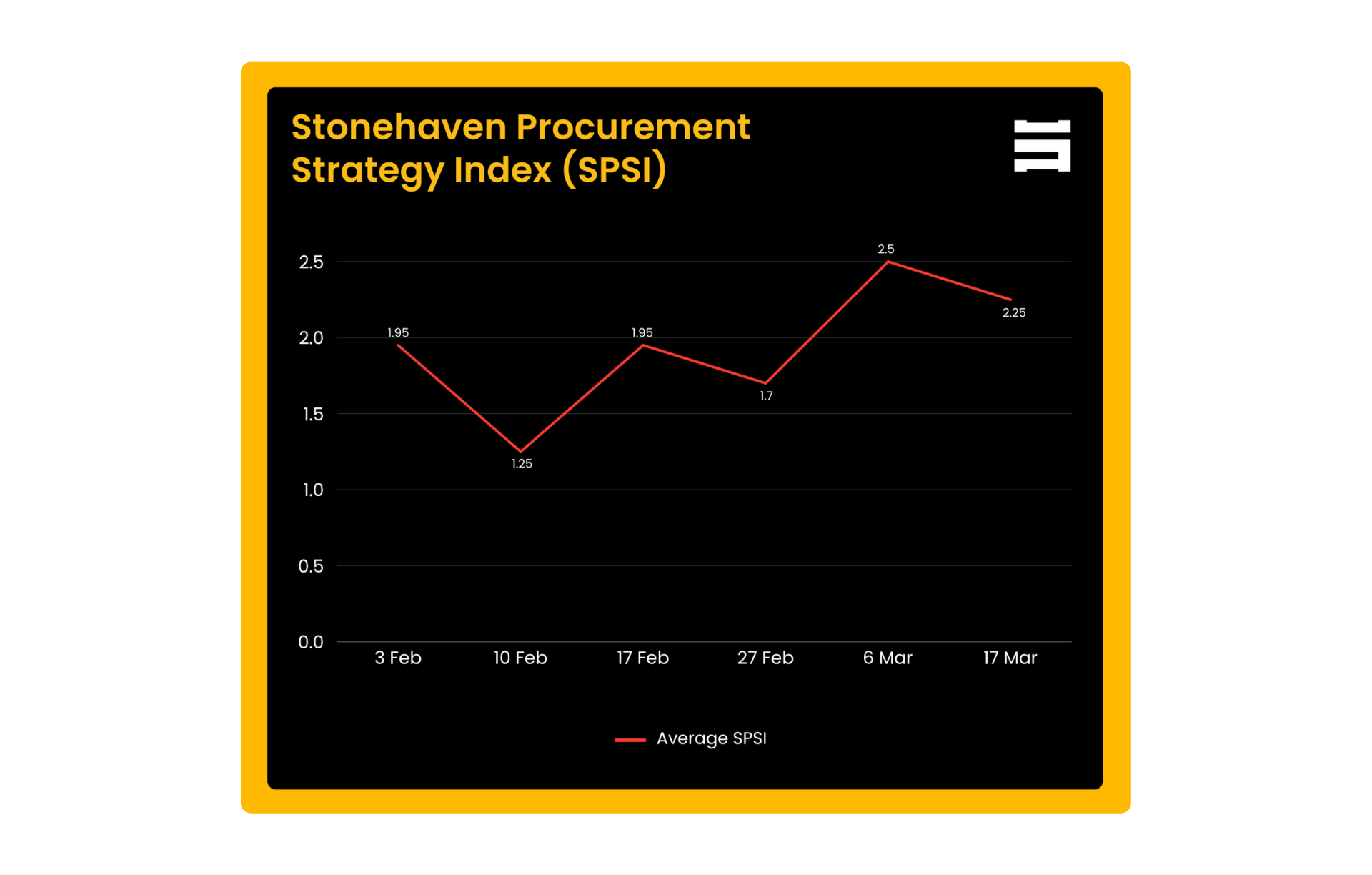

Stonehaven Procurement Strategy Index (SPSI)

The SPSI provides a simple view of current procurement risk in the construction market, based on three key factors:

-

Market Volatility (MVEI) – material price movements

-

Import & Currency Exposure (ICEI) – FX impact on imports

-

Energy & Logistics (ELEI) – fuel and freight cost pressures

The MVEI, ICEI, and ELEI sub-indices are each scored from 1 to 4, where 1 indicates stable conditions and 4 signals high risk. The composite SPSI follows the same scale:

- Below 1.5: Low risk - market stable, minimal price movement

- 1.6 to 2.24: Mild risk - minor fluctuations, monitor closely

- 2.25 to 3.25: Moderate risk - noticeable market change, selective action advised

- Above 3.26: High risk - significant instability, immediate procurement review required

Current Position (17 March): SPSI = 2.25 (Moderate Risk)

-

MVEI = 2 → mild material price movement

-

ICEI = 2 → stable currency conditions

-

ELEI = 3 → higher logistics and energy risk

Interpretation:

The market remains generally stable, but logistics and energy costs are the main risk drivers, keeping procurement conditions slightly sensitive.

Procurement Recommendation

Based on current market conditions:

-

Buy early where prices are favorable

-

Delay procurement for volatile materials

-

Monitor stable materials before committing

Recommendations for Material Purchasing

Commercial Guidance

1. Structural & Steel Packages

Steel prices show marginal upward movement, while declining zinc prices offer cost advantages in galvanized components.

Strategy:

Apply targeted cost adjustments only where required (e.g., aluminium-intensive systems), while leveraging stable HRC/CRC pricing for negotiation. Avoid blanket escalation.

2. MEP & Polymer-Based Systems

Polyvinyl continues to rise, impacting drainage, piping, and insulation systems.

Strategy:

-

Prioritise early procurement of Polyvinyl (PVC) related materials.

-

Maintain neutral pricing positions for copper and nickel-based components.

3. Energy & Infrastructure Materials

Bitumen has recorded a sharp increase, reflecting strong linkage to fuel and logistics costs.

Strategy:

-

Adjust pricing assumptions for energy-sensitive materials.

-

Monitor fuel trends before applying broad logistics contingencies.

Overall Market Position – GCC Construction

The construction market remains material-specific in its cost behavior, rather than experiencing broad inflation across all inputs.

Energy-linked and polymer-based materials continue to drive cost increases, while metals remain relatively stable with selective downward corrections. At the same time, logistics and freight conditions remain volatile and risk-sensitive, limiting any sustained cost relief in the near term.

Commercial Position

-

The market is stable but highly responsive to external drivers.

-

Procurement strategies should be targeted, timing-driven, and material-specific.

-

Contractors should avoid over-escalation and instead focus on precision-based cost planning and negotiation.

Important Disclaimer

The Stonehaven Cost Index (SCI) is provided for general information only and does not constitute a commitment, guarantee, or offer to contract at any price level. The index is based on publicly available commodity data and internal market assessments as of 17 March 2026. Actual project costs will depend on project-specific scopes, procurement routes, and commercial negotiations.

Stonehaven Project Management Services LLC accepts no liability for any loss arising from reliance on this document without appropriate project-specific advice. The index reflects indicative market movements based on weighted construction inputs and does not represent a forecast, tender price, or contractual valuation.

FAQ's

1. What is the Stonehaven Construction Cost Index and how is it calculated?

The Stonehaven Cost Index (SCI) tracks weekly price movements across key construction materials, freight indices, and currency pairs relevant to the UAE and Saudi Arabia. Data is collected every week and reviewed by Stonehaven's cost management team before publication. The index is indicative and does not constitute a tender price or contractual valuation.

2. What affects construction material prices in the Middle East?

Several factors influence construction material prices in the Middle East, including global commodity markets, shipping costs, fuel prices and currency movements. Materials like steel, copper and bitumen are particularly sensitive to international demand and logistics conditions, which directly impact construction cost trends in the GCC.

3. How often do construction material prices change?

Construction material prices can change daily depending on global market conditions. Factors such as commodity prices, shipping costs and fuel rates influence short-term movements, which is why tracking weekly construction material price updates is important for sensitive cost planning.

4. How is the Stonehaven Construction Cost Index prepared?

The construction cost index is prepared using weekly data collection across key materials, currencies and freight rates. Cost managers monitor these movements to reflect current conditions. This is then reviewed by the commercial management alongside foreign exchange and logistics trends, which influence construction pricing across the GCC before presenting to our readers.

Check Out Our Previous Issues

Talk To Our Team

Speak to our cost management specialists to benchmark, forecast, and protect your project margins, using real data from the Stonehaven Cost Index.